What to do if you’ve been in a data breach as a finance professional

Bristol James

9 Min

The finance industry is extremely susceptible to data breaches. In fact, in 2023, it was the most breached industry and accounted for 27% of all incidents handled by financial risk and advisory firm Kroll.

If you’re a finance professional and your data has been compromised, a swift and strategic response to any incursion is crucial.

In this post, we’ll outline the steps you should take (and the processes you need to be aware of) to do just that.

Step 1 – Contain the Data Breach

Once you have discovered a breach or suspect that one has occurred, immediate action should be taken to limit further damage.

Resist the urge to solve the right problem right away. Instead, focus on containment and identify the security vulnerability that caused the breach.

This process involves several key steps:

Isolate affected systems – if the breach involves workplace systems or financial platforms, isolate compromised accounts or devices from the network.

Revoke access and reset credentials – disable access for compromised accounts by resetting login credentials. Revoke permissions and ensure only authorised users can access the account.

Suspend suspicious activities – cease any transactions considered suspicious and contact other financial institutions to monitor and block potentially fraudulent activity.

Implement a temporary freeze – a credit freeze or account suspension prevents unauthorized access to sensitive data, including your credit file. This applies to personal bank accounts, payment cards, and workplace systems.

Liaise with IT and security teams – collaborate with IT and security teams to quarantine compromised systems, run diagnostics and patch security vulnerabilities.

What’s more, be careful not to destroy any evidence that may hold the key to identifying the cause (or perpetrators) of the breach later.

Assess the Situation

When a data breach occurs, it’s essential to assess the situation quickly and accurately. This involves determining the scope of the breach, the type of data compromised, and the potential impact on individuals and organizations. To assess the situation, follow these steps:

Identify the source of the breach: Determine how the breach occurred, whether it was due to hacking, phishing, or insider threats.

Determine the type of data compromised: Identify the type of sensitive information that was stolen, such as personally identifiable information (PII), financial data, or confidential business information.

Assess the scope of the breach: Determine the number of individuals and organizations affected by the breach.

Evaluate the potential impact: Consider the potential consequences of the breach, including financial loss, reputational damage, and identity theft.

By assessing the situation quickly and accurately, you can take prompt action to mitigate the damage and prevent further unauthorized access to sensitive information.

Secure Your Operations

Securing your operations is critical to preventing further data breaches and protecting sensitive information. To secure your operations, follow these steps:

Update passwords and PINs: Change passwords and PINs for all affected accounts, including financial accounts, online accounts, and mobile devices.

Implement good password hygiene practices: Use unique and complex passwords, avoid reusing passwords, and change passwords regularly.

Enable two-factor authentication (2FA): Require a second factor, such as a code sent to a mobile device or a biometric scan, in addition to a password to access sensitive information.

Monitor accounts: Regularly monitor financial accounts, credit reports, and online accounts for suspicious activity.

Use encryption: Use encryption to protect sensitive data, both in transit and at rest.

By securing your operations, you can prevent further unauthorized access to sensitive information and reduce the risk of identity theft and financial loss.

Step 2 – Verify the breach

If you’ve received notification of a breach, it is important to verify the notification’s authenticity. This step can be performed in parallel with step one. This step is crucial for data breach victims to ensure they are taking the right steps to protect their information.

Why is verification necessary?

Scammers frequently use fake breach alerts in phishing scams. Therefore, it’s important to contact the entity involved (via official channels such as their customer service number or website) to confirm that the breach notification is authentic.

To verify whether your email has been compromised, you can also use eftsure’s Data Breach Checker and receive additional tips and advice on how to protect data.

Step 3 – Assess the breach of sensitive data

Step three involves assessing the data breach, whether it’s a small incident or a massive data breach, to help understand the risks it poses and how those risks can be mitigated.

Gather as much information about the breach as possible and do so while the details are fresh.

Each assessment should cover:

The types of personal or company information compromised.

The circumstances, cause and extent (if known) of the breach, and

The nature of any harm to individuals or the business (such as data loss) and whether harm can be removed or reversed with remedial action.

Step 4 – Comply with internal reporting protocols

All data breaches require swift internal communication to minimise the risk of further exposure, but this is particularly important in finance. This is particularly important in finance, where multiple data breaches can have compounded effects on both the organization and its clients.

Reports make management, legal and security teams aware of the breach so that further action can be taken. The protocols themselves also clarify how breaches are documented, investigated and reported to third parties.

The consequences of non-adherence can be immense. In 2017, credit agency Equifax suffered a data breach that exposed the personal details of around 163 million people.

Notifying affected parties is a critical step in responding to a data breach. This includes notifying individuals whose sensitive information was compromised, as well as relevant authorities and regulatory bodies. To notify affected parties, follow these steps:

Identify affected individuals: Determine which individuals had their sensitive information compromised in the breach.

Notify affected individuals: Notify affected individuals in writing, providing them with information about the breach, including the type of data compromised and the steps they can take to protect themselves.

Notify regulatory bodies: Notify relevant regulatory bodies, such as the Federal Trade Commission (FTC) and state attorneys general, about the breach.

Notify credit bureaus: Notify the three major credit bureaus (Equifax, Experian, and TransUnion) about the breach, and request that they place a fraud alert on affected individuals’ credit reports.

By notifying affected parties, you can help prevent identity theft and financial loss, and demonstrate your commitment to protecting sensitive information.

Step 4 – Change passwords and enable two-factor authentication (2FA) for online accounts

As a finance professional, you may manage multiple accounts such as workplace systems, banking platforms and investment accounts.

In step five, monitor the above-mentioned accounts for suspicious activity on an ongoing basis, and consider using credit monitoring services to automate this process. Update the passwords for each (and not just those directly impacted by the breach) and remember to do so with robust password hygiene.

Also enable two-factor authentication (2FA) where possible to ensure that hackers cannot access other areas of compromised systems.

Step 5 – Monitor accounts with credit monitoring

In step five, monitor the above-mentioned accounts for suspicious activity on an ongoing basis since criminals may wait weeks or even months before they act.

Reporting the breach promptly can help mitigate the risk of identity thieves exploiting the compromised information.

Financial systems, internal databases and client accounts.

Corporate financial records and strategic financial plans, and

Tax forms and other compliance-related documents.

Step 6 – Report the breach

If the breach impacts banks, credit card providers, investment firms or other customers, it should be reported to them as soon as possible. It’s also vital to discuss remediation options and be upfront and transparent about what data was compromised.

Notify credit bureaus: Notify the three major credit bureaus (Equifax, Experian, and TransUnion) about the breach, and request that they place fraud alerts on affected individuals’ credit reports.

The NDB scheme

In Australia, the Notifiable Data Breaches (NDB) scheme requires organisations with more than $3 million in annual turnover to report data breaches if there potential to cause serious harm to affected individuals. A report must also be sent to the Office of the Australian Information Commissioner (OAIC). In addition to notifying the OAIC, it is also important to notify the three credit bureaus to ensure comprehensive protection for affected individuals.

In the notification process, organisations must consider:

Their obligations and responsibilities under the NDB scheme (stipulated in the Privacy Act 1988).

How notification should occur. This includes what information is provided, how the notification will be provided and who is responsible for notifying the affected individuals.

Who else other than affected individuals and the OAIC should be notified.

Whether the breach triggers reporting obligations to other entities, and

Whether it is appropriate to consult with law enforcement before details of the breach are made public.

Step 7 – Beware of phishing attacks targeting data breach victims

Phishing attacks are a common precursor to data breaches, but in some cases, the process is reversed.

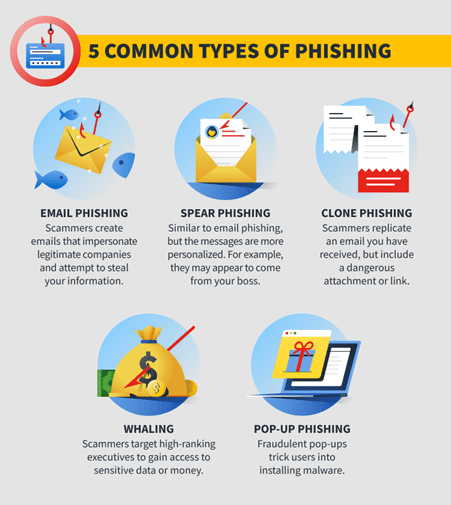

After a data breach, compromised data may then be incorporated into targeted phishing attacks such as:

Spear phishing – where personalised emails or messages tailored to specific individuals persuade them to reveal sensitive information.

Whaling – a type of spear phishing where high-level executives and decision-makers are targeted. Emails may contain urgent requests for wire transfers from other executives to appear more credible.

Clone phishing – where criminals clone a legitimate email and make an identical version with malicious links or attachments. This is effective after a data breach since criminals know who you’ve been communicating with.

Business email compromise (BEC) – here, attackers compromise a legitimate business email account and use leaked information to pose as a colleague. Attacks then send fraudulent emails disguised as routine business requests.

Some of the varied phishing attack types you need to be aware of (Source: Armour Zero)

Targeted phishing attacks are particularly dangerous after a data breach because they exploit the trust and familiarity associated with legitimate communications. This is why it’s crucial to remain vigilant for suspicious activity in the period after a data breach.

Step 8 – Strengthen cybersecurity measures

Once a breach has been identified and properly remediated, the strengthening of cybersecurity measures becomes a priority.

Here are just two of the actions you can be involved in.

1 – Update firewalls and antivirus software

Cybercriminals often exploit outdated security devices to infiltrate networks, so keep your defences current to block malicious activity.

In finance, robust firewall configurations and proactive malware detection are essential. Set up automatic updates for security solutions so that your details (and the business’s assets) are better protected against the latest threats.

2 – Training and education

Training employees on cybersecurity best practices is essential to prevent future incidents. Staff should be encouraged to develop a security-first mindset that can:

Recognise phishing attempts.

Avoid risky online behaviour, and

Understand the importance of keeping software and systems updated.

Education also helps foster the sort of workplace culture where staff are encouraged to immediately report data breaches to their superiors.

To sum up

If you’ve been involved in a data breach as a finance professional, the importance of swift and decisive action cannot be understated.

Start by confirming the validity of the breach and check for compromised email addresses with eftsure’s Breach Checker tool. Then it is a matter of changing passwords, enabling two-factor authentication and monitoring the relevant accounts for suspicious activity.

Regularly check your credit report to detect any unusual activity and take prompt action if necessary.

In the aftermath of a breach, be wary of increased phishing activity and ensure that you’re following recognised internal and external reporting protocols.

By following these steps, you can play your part to protect the company’s assets and the personal information of its staff and customers.

Call back procedures are among the most important measures to mitigate your organisation’s exposure to the risk of fraud. Unfortunately, call-back controls …

When implementing or designing financial controls within Accounts Payable (AP), every CFO should start by asking themselves this question: are our financial …

Eftsure provides continuous control monitoring to protect your eft payments. Our multi-factor verification approach protects your organisation from financial loss due to cybercrime, fraud and error.