Finance glossary

What is source-to-pay (S2P)?

Source-to-pay (S2P) is an end-to-end process in procurement that encompasses the activities associated with sourcing products from suppliers.

Fraud prevention is a strategic approach to identifying and combatting fraudulent transactions, safeguarding financial systems, and preventing fraudulent activities that could lead to financial loss or reputational damage.

Just about every business transaction is now digital, therefore businesses are facing fraud at higher rates and experiencing greater fallout when fraudulent acts are successful.

Closely linked with cybersecurity, fraud prevention isn’t something that humans can do alone. In order to keep up with technology-led fraud, using technological tools to flag suspicious behavior, encrypt sensitive data, and closely monitor secure transactions is a must. Fraud is always changing, and as such, the tools available for businesses to use to prevent fraud are always changing, too.

Staying on top of your organization’s fraud prevention program is about more than stopping fraud before it happens; it’s about illustrating to customers, business leaders, and stakeholders that trust and security are key pillars in your company.

Not only are businesses at risk of being exposed to fraud but individuals can also get caught in the crosshairs of these schemes. Some of the most common types of fraud today are:

When someone uses a stolen credit card or stolen credit card information to make a purchase, they are committing fraud. Because payments can be made in-person, online, and over the phone, it can be hard for businesses to catch credit card fraud. Verifying the buyer’s identification, as well as tracking location details of the user and of the credit card itself can help stamp out credit card fraud.

If a person inside of an organization is inflating revenue numbers, mis-categorizing expenses, or trying to hide historical transactions altogether, accounting fraud is happening. Accounting fraud is incredibly serious; it has taken down large companies and had massive negative impacts on the global economy when it happens at scale.

Identify theft can happen in many different settings, but anytime someone uses another individual’s information — such as their name, address, Social Security number, or credit card details – without their permission, it’s considered identity theft. Identity theft can be used to lie to the federal tax authority, open new lines of credit, or make large purchases.

Everyone knows the story of a struggling business owner who tries to burn down the shop and get money from the insurance claim, right? If not, it’s a classic attempt at insurance fraud. Insurance fraud can be executed on an individual level, such as trying to get health insurance coverage after a major injury takes place, or on an enterprise level as described above.

Looking at digital fraud, malware attacks are used by hackers to infect computer systems and business networks with viruses such as ransomware or spyware. These viruses can corrupt the systems entirely, expose sensitive information, and lead to businesses going belly-up if they can’t recover from the attack.

Another cybersecurity attack that everyone needs to watch out for is phishing. Phishing emails can trick even the smartest employees into changing payment information for certain transactions, sending large sums of money to hackers, and entering their login credentials into a fake website. Employee training and building a culture of open communication are two of the best ways to prevent damage from phishing attacks.

The best fraud protection solutions are two-pronged, consisting of both fraud prevention and fraud detection activities. Although the terms sound similar, they are slightly different, and the difference is worth highlighting.

Fraud prevention solutions are best practices, systems, and additional safeguards that are meant to stop fraud attacks before they occur. By reducing the risk of future fraud, businesses can focus more on business growth and other priorities, instead of cleaning up fraud-related disasters down the line.

Fraud detection, on the other hand, happens during a fraud attempt. For instance, if a hacker is using a bot to test out thousands of different platform login credentials to break into a business system, some fraud detection tools can flag that behavior and send an alert to the leadership team, giving them time to respond before the attempt is successful. Detection is more about mitigating fraud when it’s happening, while prevention focuses on stopping fraud from happening in the first place.

A robust fraud prevention solution stops fraud risk before it starts. Because of the impact that fraudulent activity can have – no matter where it originates from – the best approach to mitigating those risks is through fraud prevention. Big or small, businesses of all sizes are major targets for hackers and fraudsters. Some hackers may want to gather and sell customer information while others want to stop manufacturing plants from working and hold a company for ransom. So, if such a wide range of fraud risks exist, can you actually do anything to prevent them? The answer is a resounding “Yes!”

Strong internal controls aren’t just for accounting teams and financial processes; implementing internal controls throughout the organization can lead to heightened accountability and transparency surrounding key transactions or priorities. With strict access controls to sensitive data sets and a clear segregation of duties, it’s harder for employees to commit fraud and easier for them to avoid it altogether. Not only is it important to implement strong internal controls, finance professionals should be pressure testing these controls periodically to ensure due process is being followed and organisations are always protected against fraud attempts.

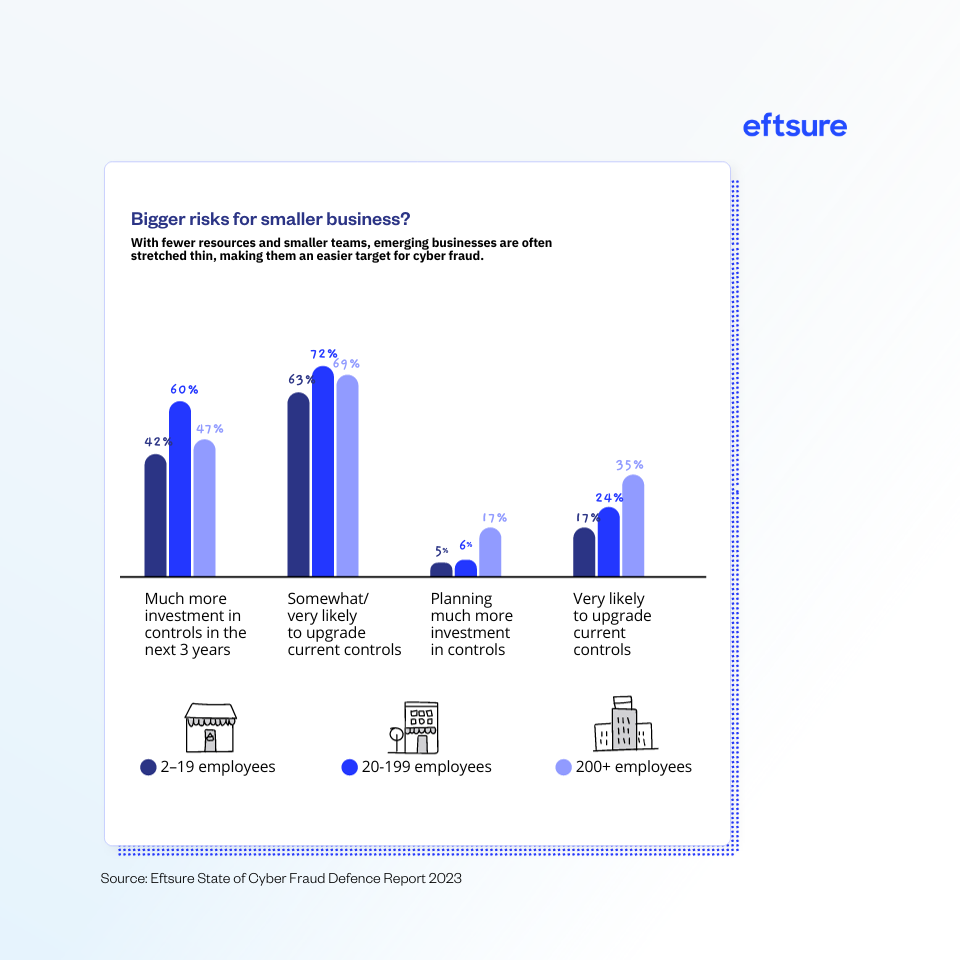

In a our recent State of Cyber Fraud Defence Report, we looked at the risks for small businesses versus large organisations and assessed their likelihood to invest in new fraud prevention controls:

Some companies have knowledgeable IT teams within the organization, but for many businesses, that’s not the case. Because of the constantly changing threats in the technology space, being able to access an expert resource for system architecture needs, security measures, and next-generation fraud prevention tools is non-negotiable. Because internal IT teams are costly and can take a while to construct, consider working with a managed service provider that has experience in serving businesses in your industry.

Specialized fraud prevention software is one of the best ways for businesses to insulate their operations from hackers and bad actors. Because computer-based solutions can work faster than humans, these software tools can process thousands of records in an instant, acting as a final line of defense before an act of fraud takes place.

Accounts payable teams are a key target for fraudsters. Our technology specialises in B2B payment protection to mitigate the risks of payment errors, fraud and cybercrime. Safeguarding $216B in payments annually, Eftsure is trusted to verify vendor identities, validate bank account information, monitoring compliance requirements, and protecting payments from end-to-end.

All businesses should give their employees access to a safe reporting hotline where they can alert leadership about fraud threats directly. Simply having whistleblower hotlines in place will remind fraudsters that they won’t easily get away with their schemes. Even further, reporting mechanisms within an organization will help a culture of trust and transparency flourish. When employees know they can highlight risks without fear of retaliation, they’re much more likely to take action when it comes to it.

Whenever a business adopts a new tool or implements a new fraud prevention solution, employee training is paramount. If internal teams don’t know how to support effective fraud prevention, then they won’t. Because things change often, fraud-related trainings should take place at least once a year, if not more.

Conduct thorough due diligence on vendors, suppliers, and business partners to verify their legitimacy, financial stability, and reputation. Establishing clear contractual terms, conducting periodic reviews, and monitoring vendor activities can help prevent fraudulent schemes such as billing fraud, kickbacks, or procurement fraud.

Uncovering fraud isn’t always easy, but with the right strategies in place, organizations can cut down on the time it takes to identify malicious behavior, saving time and downstream costs associated with recovery after an attack. Some of the best ways to detect fraud while it’s happening are:

There is a plethora of advanced software solutions that are built specifically for fraud detection. These tools rely on fraud detection algorithms, anomaly detection, and machine learning models to identify behavior that is out of the ordinary.

Audits are not the most glamorous method of detecting fraud, but there are plenty of instances where routine accounting audits pick up fraud attempts. By auditing financial transactions, business systems, and payment information closely, organizations can detect fraud in real time. In order for audits to be effective at fraud detection, the auditors need to be different from the people who own the tasks or systems that are being audited. If that’s not the case, a dangerous conflict of interest is at play.

Detecting fraud risks is everyone’s responsibility. With proper training and a clear understanding of what fraud can look like within their day-to-day roles, employees at all levels can serve as impressive fraud detectors.

Fraud prevention solutions will simply never work if only one person within a company is prioritizing them; fraud prevention is a team effort. Every person plays a part, including:

Benefits of prioritizing effective fraud protection

Hopefully, your organization never experiences the negative impacts of fraud, but if you’re looking for some encouragement as to why businesses should prioritize a robust fraud prevention solution, here are some of the benefits of doing just that:

Summary

Source-to-pay (S2P) is an end-to-end process in procurement that encompasses the activities associated with sourcing products from suppliers.

Reading a check may appear straightforward at first glance, but the various elements that comprise a check play a crucial role in …

A hedging strategy is a risk management strategy to avoid large financial statement losses due to investment fluctuations. Hedges work like an …

Eftsure provides continuous control monitoring to protect your eft payments. Our multi-factor verification approach protects your organisation from financial loss due to cybercrime, fraud and error.