However, taxing authorities do not follow GAAP. For tax reporting purposes, businesses can use accelerated depreciation, which allows more of the cost to be expensed in the year placed in service. In addition to accelerated depreciation deduction methods, there are also special depreciation options that further increase the depreciation expense deduction. Using an accelerated depreciation method gives business owners the ability to lower taxable income to preserve profitability.

Types of Depreciation Methods

Businesses have options when it comes to the standard depreciation methods used. However, most companies lean toward straight line depreciation for book purposes and MACRS for tax purposes. Nevertheless, here are some other common depreciation methods:

Straight Line Depreciation

Straight line depreciation is one of the simplest depreciation methods for book purposes. The straight line depreciation method takes the cost basis minus the salvage value and divides that number by the asset’s useful life. The salvage value is the amount of money the company expects to sell an asset for at the end of its useful life. Since this number can be hard to determine, many companies do not include it in the calculation.

Let’s say that you purchase an asset for $10,000 with an estimated useful life of five years. In the first full year, you would write off 20% of the asset as depreciation expense, which is found by dividing one by five. Next, multiply the straight line depreciation rate by the cost basis, resulting in a depreciation expense of $2,000.

Units of Production Depreciation

Units of production depreciation is commonly used in manufacturing businesses that produce units. This method takes the number of units produced during the period divided by the total number of units the asset will produce over its useful life. Then, this rate is multiplied by the asset’s book value.

Let’s say your machine is expected to produce 10,000 units before it is no longer usable. In the current year, your machine produced 2,500 units. Dividing 2,500 by 10,000 results in a 25% depreciation rate. If your asset’s book value is $10,000, you would record $2,500 in depreciation expense.

Modified Accelerated Cost Recovery System (MACRS) Depreciation

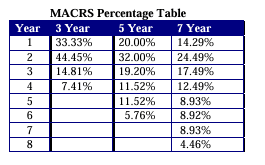

MACRS is the preferred depreciation method for tax purposes. This method uses tables released by the IRS to determine the applicable depreciation rate. Below is an example of the MACRS table:

Keeping the same facts as our previous examples, let’s say you purchased a five-year asset for $10,000. Using the MACRS table, we find that the first-year depreciation rate for a five-year asset is 20%, resulting in a depreciation deduction of $2,000.

Types of Accelerated Depreciation Methods

Accelerated depreciation methods generate greater depreciation deductions in the first few years compared to straight line depreciation and MACRS. Here are two accelerated depreciation methods:

Double Declining Balance Depreciation

Double declining balance depreciation writes off the cost basis of the asset twice as fast. To calculate this depreciation deduction, double the straight-line depreciation rate and multiply the amount by the book value balance.

Let’s say that your straight line depreciation rate is 0.20% and the asset’s book value is $10,000. Doubling the 0.20% would result in a 0.40% deduction. Multiplying this by $10,000 results in a $4,000 depreciation deduction.

Sum of Years’ Digits Depreciation

The sum of years’ digits accelerated depreciation method calculates depreciation by dividing the remaining estimated life by the sum of years’ digits. The sum of years’ digits is found by adding each year of useful life together.

Let’s say the asset has a five-year useful life and cost $10,000. The sum of years’ digits would be 1 + 2 + 3 + 4 + 5, which equals 15. In the first year, the asset still has five years of remaining life. This means the depreciation rate would be 5 / 15 or 33.33%. Multiplying this by the assets cost basis of $10,000 results in a $3,333 depreciation deduction.

Special Accelerated Depreciation Deductions: Bonus and Section 179

Two other types of accelerated depreciation deductions are Bonus depreciation and Section 179 depreciation. These methods are considered special depreciation deductions and are only available as a tax deduction. Let’s break down the components of these two items in more detail.

Bonus Depreciation

Bonus depreciation allows businesses to write off a fixed amount of assets placed in service during the year. However, under the 2017 Tax Cuts and Jobs Act, bonus depreciation has begun to phase out. For the 2024 tax year, businesses can use this method to depreciate 60% of an asset. In 2025, this amount is reduced to 40%. Then, in 2026, the percentage drops to 20% with full phase out by the 2027 tax year.

One of the main stipulations for Bonus depreciation is that the asset must be placed in service before year-end. For example, a piece of machinery must be up and running before year-end to be eligible. Let’s say you placed a $10,000 asset in service during the year. Under Bonus depreciation, you could take a $6,000 tax deduction.

Section 179

Section 179 depreciation is another type of special depreciation option that allows you to expedite your depreciation expenses. Under this method, you can write off 100% of certain assets placed in service before year-end. This includes machinery, equipment, office furniture, and qualified leasehold improvements.

One of the caveats of Section 179 is that the depreciation deduction cannot create a net loss. For example, if you only have $6,000 of taxable income and place an eligible $10,000 asset in service, your depreciation deduction is limited to $6,000.

The Advantages of Accelerated Depreciation

There are advantages of using accelerated depreciation to unlock a higher depreciation deduction. For one, it helps you lower your taxable income. By expediting your deductions, you can lower taxable income. However, it’s important to understand that accelerated depreciation is a deferral method. Your depreciation expense will be lower in subsequent years.

In addition, special depreciation options allow you to avoid minimal deductions for assets placed in service at the end of the year. Depreciation is pro-rated based on when the asset is placed in service. For example, straight line depreciation takes 20% for a full year of depreciation, but if your asset isn’t in service until July, your deduction is limited to 10%.

The Disadvantages of Accelerated Depreciation

One of the main disadvantages of accelerated depreciation is depreciation recapture. Depreciation reduces your basis in the asset. Let’s say you took $6,000 of depreciation on a $10,000 asset. This generates a cost basis of $4,000. If you were to sell the asset for $7,000, you would need to pick up $3,000 of depreciation recapture.

Additionally, certain assets aren’t eligible for accelerated depreciation. For one, rental property depreciation requires a 27.5 useful life for residential property and 39 years for commercial properties. Real estate is not eligible for accelerated or special depreciation options.

Summary

- Depreciation is the process of reducing an asset’s basis over its estimated useful life.

- Examples of standard depreciation methods include straight line, units of production, and MACRS.

- Examples of accelerated depreciation methods include double declining balance and sum of years’ digits.

- Examples of special depreciation options include Bonus depreciation